July 15, 2025

Elevated mortgage rates. Limited inventory. Rising prices.

Many headlines about today’s housing market elicit feelings of uncertainty. For those who lived through the housing crash of the 2000s, it’s easy to compare what they are reading today to what occurred nearly two decades ago.

However, here’s the good news: Today’s market is built on a much stronger financial footing than the one that led to the 2008 crash, according to NewHomeSource. NewHomeSource is a platform for new home listings with homebuilder reviews.

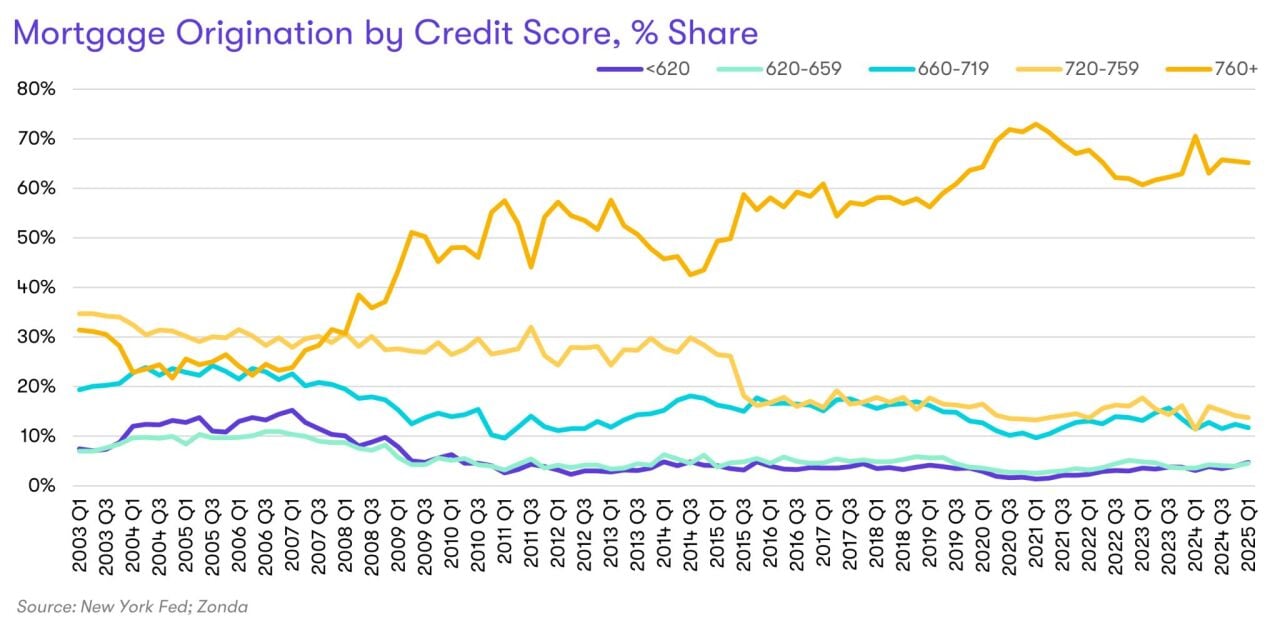

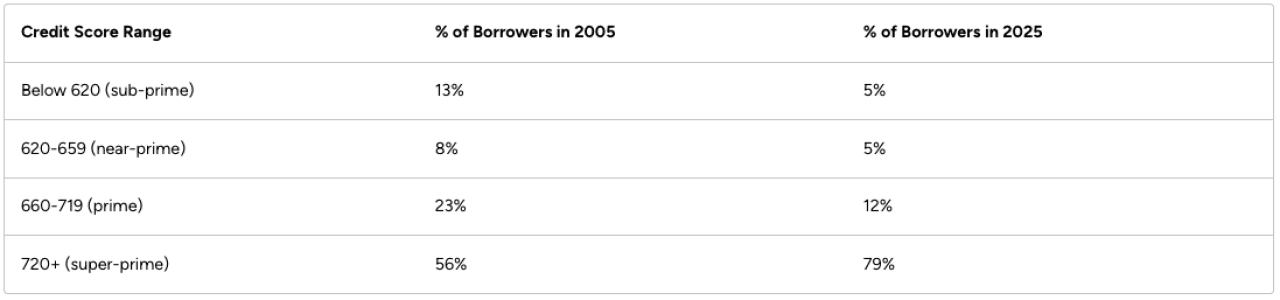

As an illustration, here are the credit scores of mortgage borrowers in 2005 and 2025:

In 2005, many below-prime loans had risky terms with minimal documentation or little money down. Following the housing crash of the 2000s, lenders and regulators implemented significant changes. Risky loans with minimal documentation and little money down are far less common in 2025.

“It’s easy to get spooked with all the headlines about the changing housing market,” says NewHomeSource chief economist Ali Wolf. “It’s important, though, to think about the market rationally. The housing market is certainly different than it was just 12 months ago: Buyers now have negotiating power, and sellers have to be flexible. But fundamentals matter. The basis of today’s market is much more solid than the housing boom we saw in the mid-2000s.”

What Does This Mean for Buyers?

The market is on much stronger footing. Today’s lending environment is built on stronger financial fundamentals. Fewer risky loans mean fewer defaults. Fewer defaults mean less vulnerability to the kind of collapse seen in 2008.

Credit scores matter more than ever. With mortgage rates elevated, a good credit score can lead to real savings. Better credit typically unlocks lower rates, broader loan options, and a smoother approval process. It can even be the difference between qualifying for a loan or not.

Other buyers are more qualified, too. If you are shopping for a home, you are more likely to compete against other financially secure buyers. Coming in prepared — with preapproval, savings, and a solid credit score — can help you stand out and stay competitive.

Bottom Line:

While it’s useful to track macro trends for context, the housing market ultimately comes down to one thing: you. Your personal finances ultimately determine what’s possible for you.

Whether you plan to buy soon or are just keeping an eye on the market, it never hurts to check in on your credit. The stronger it is, the more options you will have when you come across the right home.

This story was produced by NewHomeSource and reviewed and distributed by Stacker.

RELATED CONTENT: Dream of Homeownership But Afraid Of The Credit Check? These Mortgage Lenders Can Handle Bad Scores.